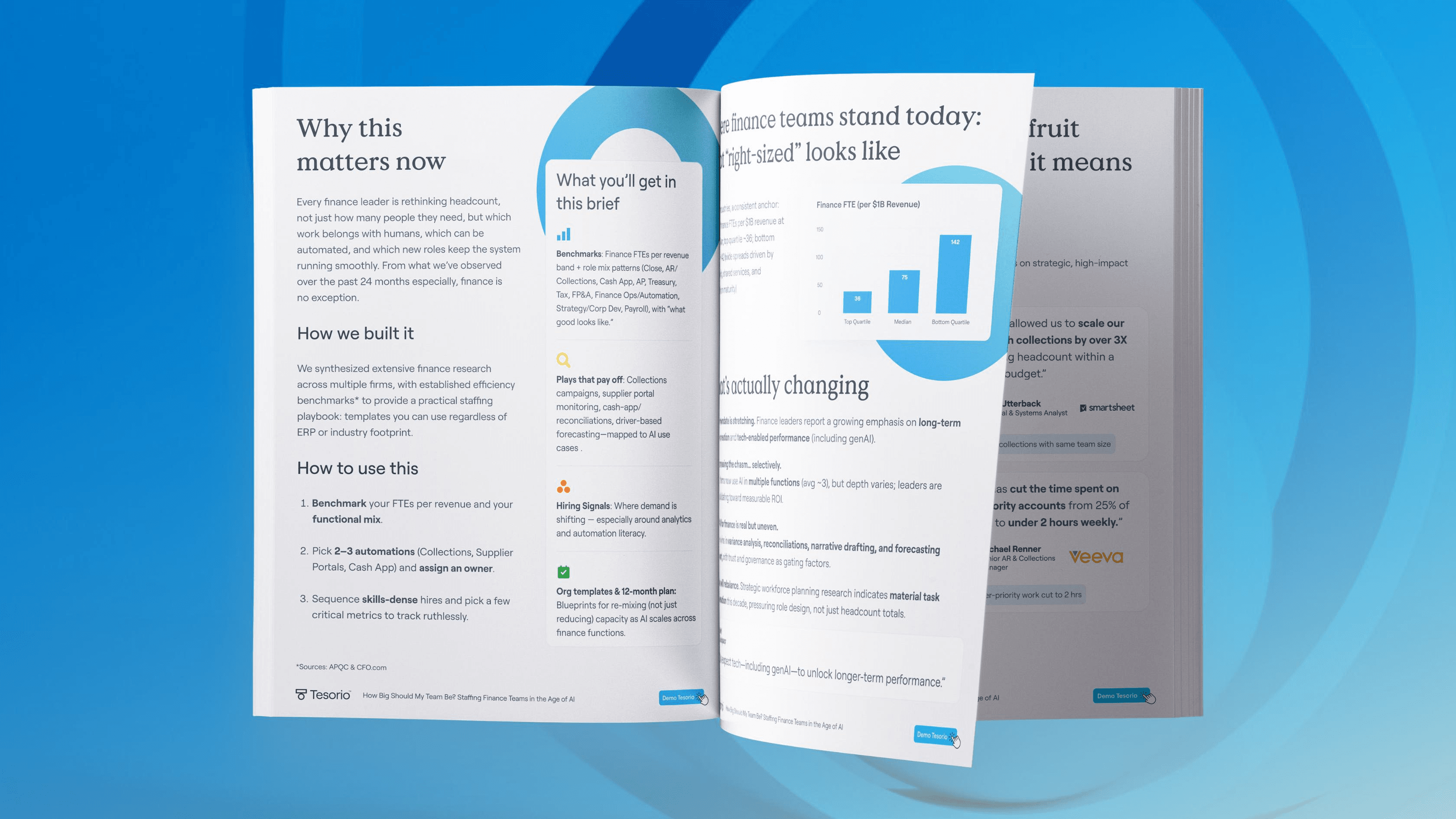

DSO = Days Sales Outstanding

DSO = Days Sales Outstanding DSO is a metric typically used by Chief Financial Officers (CFOs) in board meetings to show the status of, or hopefully an improvement in a company’s cash conversion cycle. Days Sales Outstanding is one of the most critical and commonly used metrics for B2B collections, accounts receivable (AR), and finance teams in general. It’s important to understand how DSO works in order to interpret it properly and understand when DSO may actually be a misleading indicator.

CFOs, finance teams in general, and accounts receivable teams in particular, use Days Sales Outstanding to illustrate how cash is flowing into the business. Understanding how to calculate DSO and interpret the results is key to setting your company’s cash flow expectations.

Days Sales Outstanding In A Nutshell

DSO measures the average number of days a company requires to receive cash after it makes a sale. Companies may report DSO on a monthly, quarterly, or annual basis. Monthly reporting of DSO is fairly onerous unless the calculations are highly automated with a company’s Enterprise Resource Planning (ERP) system connected with finance intelligence systems that automatically track DSO. Using spreadsheets to calculate DSO is possible, but monthly calculations will be a painful and time-consuming process.

The most basic way to calculate DSO is to divide the total value of all your accounts receivable during the reporting period by the total value of all your credit sales made during that same period. Then you multiply that result by the number of days in the period.

The Basic Formula for Days Sales Outstanding is as follows:

DSO = (Accounts Receivable/Total Sales) * Number of Days

There are other DSO formulas that may give you a more accurate indication of the health of your collections and AR processes. We will review those in another blog post.

Why DSO Matters

DSO is a proxy for collections velocity and finance teams, not to mention CEOs, who want to collect outstanding accounts receivable as fast as possible. The benefits of faster collections are tremendous:

- Better free cash flow

- Less reliance on expensive credit and trade financing

- A more liquid balance sheet

- Higher limits and better terms on credit

- Higher operating profits and operating margins

- Less overall business risk

- Higher company valuations

- Happier sales teams

Ultimately, companies with a better DSO number generally have a higher sustainable growth rate, a better Cash Conversion Cycle, and stronger returns. This leads to the growth of wages, profits, and dividends. Companies with better DSO numbers can afford to think more strategically and continually invest in their business.

Note: Some companies even manage to collect cash before they have to pay their bills; Apple and Amazon are two notable examples of companies that actually have a negative cash conversion cycle. In other words, they can hold receivables in an interest-bearing account until they need to pay suppliers. Curiously, this has no impact on DSO because cash sales are not counted in DSO calculations.

How to Interpret Days Sales Outstanding

Directionally, a high DSO number is bad and a low DSO number is good. Exact magnitudes vary by industry so it’s important to track these metrics relative to your peers. A higher DSO number than peers indicates that a company is selling to customers on less advantageous credit terms, collections are taking more time, and accounts receivable is not an efficient process. Longer spans than expected between the time of sale and time of payment can lead to a range of cash flow problems.

DSO Does Not Include Cash Sales

Remember - the formula for calculating DSO only counts credit sales. Cash sales are not factored into DSO because there is no time between a sale and payment. For this reason, a company that has a very high proportion of cash sales could actually have a higher (and apparently less healthy) DSO than companies that collect cash more slowly. That’s because a company that issues credit on 100% of sales and has a DSO of, say, 20, could have significantly worse free cash flow than a company with a DSO of 60 that only issues credit on 30% of its sales.

DSO Is Only An Average

DSO is an average and it may hide considerable variations that can impact financial planning and collections forecasting. For seasonal businesses, for example, DSO may swing dramatically up and down depending on industry convention. Additionally, if collections are clustered in the span of a week, this could make operating cash flow very lumpy. In theory, it should normalize out. In practice, big variances within the averages can cause considerable stress on companies.

DSO Changes Could Mean A Number of Things - Sometimes Conflicting

When a company sees DSO moving one way or another, there could be various causes. If DSO becomes smaller, a company may be tightening payment terms or it may have signed a very large customer that is paying on better terms. It also could mean that a company has written off a chunk of bad debt, which would actually boost DSO. If DSO goes down, but so does sales, then it's a fair question to ask whether the company is restricting credit too tightly, to the detriment of top-line revenue. Conversely, if DSO goes up (gets worse), this could indicate customers are struggling to pay (in a recession or downturn), or merely that vendors are aggressively stretching out their payment terms. This is particularly common when smaller companies are selling to larger companies - and it’s an accepted method for larger companies seeking to improve cash flow and reduce working capital.

A Sharp Spike In DSO Can Mean Big Problems

This can be an indicator of an impending cash crunch. Any significant degradation of DSO should kick off an immediate plan to rapidly boost collections efforts to try to get ahead of the problem. Additionally, any DSO spike should kick off a detailed, cross-functional analysis of what is happening with customers to try to better understand and dissect the cause. For instance, a DSO spike could mean that the credit team has been issuing credit to customers that are not credit-worthy.

Conclusion: Days Sales Outstanding Is A Good Start

DSO is a good basic indicator of the health of your collections processes and your cash flow performance. Any company that is a serious cash flow performer will most likely have an industry-leading DSO. That said, DSO can only tell part of the story. A host of other metrics, including 90 Day Aged, Average Days Delinquent and weighted DSO, can provide an even more nuanced picture of your collections and AR processes - and give you deep insights into how to turn the knobs and pull the levers available to influence your free cash flow and cash flow performance.